Laredo sits on the border between the US and Mexico. While international travel can lead to congestion on the city’s major highways, the roads in Laredo are fairly peaceful, and crime rates are relatively low.

This likely contributes to the area’s low car insurance rates—drivers pay around $86 a month for car insurance on average. But rising inflation costs and supply chain shortages are causing rates to go up nationwide, so you may need to shop smart to keep your Laredo car insurance costs low.

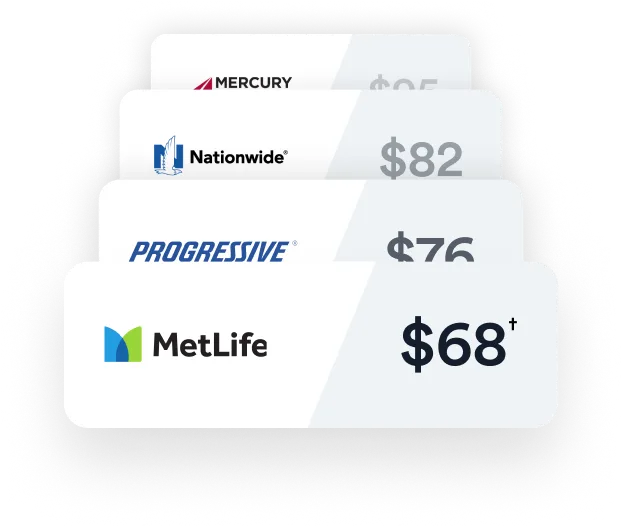

Average cost of car insurance in Laredo, TX

On average, drivers in Laredo pay about 11% less for car insurance than the Texas state average and about 36% less than the national average.

This table shows the average monthly cost of car insurance coverage for the city of Laredo, the state of Texas, and the US as a whole.

| Coverage type | Laredo | Texas | United States |

|---|---|---|---|

| Full coverage | $91 | $131 | $150 |

| Minimum coverage | $34 | $53 | $61 |

| All coverage | $86 | $97 | $114 |

The best car insurance companies in Laredo, TX

Insurance companies all have a unique way of assigning risk based on your driving profile, which means you could pay very different prices from one insurer to the next. The only way to be sure you’re getting the cheapest car insurance available to you in Laredo is to compare rates from multiple insurance companies before you buy.

Let’s take a closer look at a few companies that were rated highly by drivers in South Texas.

Jerry score: 4.5 stars

AM Best rating: A-

Clearcover’s easy-to-use mobile app is great for digital-savvy customers who want a hassle-free experience. Their rates are among the lowest in the Laredo area, and they’re especially well-known for offering affordable insurance to customers who have a less-than-perfect driving record.

Jerry score: 4.3

AM Best rating: A

Mercury’s low prices and convenient coverage options make them a South Texas favorite. Customers especially love that Mercury offers mechanical breakdown insurance and rideshare coverage.

Jerry score: 4.3

AM Best rating: A+

Nationwide’s customizable policies, wide range of discounts, and easy-to-use mobile app make them a great choice for most drivers. Most shoppers find low prices with Nationwide, especially drivers with poor credit who may struggle to find affordable premiums elsewhere.

Jerry score: 4.5

AM Best rating: A

Safeco’s low prices and top-notch customer service make them a solid favorite in the Laredo area. They also offer a variety of coverage options, so it’s easy to customize your policy.

Recent trends in Laredo car insurance prices

Car insurance prices in Laredo are somewhat lower than the Texas state average, but they could be on the rise. Let’s look at a few factors that impact Laredo car insurance costs.

Inflation

According to a report by S&P Global Market Intelligence, car insurance rates have gone up 11.5% in Texas in 2023.1 Inflation is a big part of the reason why.

In recent years, inflation has caused medical expenses and vehicle repair costs to skyrocket. That means insurers have to pay out more for claims—and they pass those costs on to consumers.

Crime rates

In 2009, Laredo was named the “Most Unsafe City for Stolen Vehicles.” In an effort to turn this around, the city created the Laredo Auto Theft Task Force, which has helped bring auto theft rates down significantly.2 3

Insurers charge more for car insurance in areas where motor vehicle theft is high, so the ATTF has almost certainly had an impact on bringing rates down for Laredo drivers.

That said, auto thefts are on the rise nationwide, and some reports indicate that they’re increasing in Laredo as well.4 This could lead to an increase in car insurance costs in the near future.

Traffic

Despite I-35 being a major international corridor, traffic in Laredo is relatively smooth. Less congestion on the roads means less of a chance of getting into an accident, which could be a factor in why Laredo’s car insurance costs are lower than average.

However, an increase in severe car accidents in Laredo could lead to insurance costs going up over the next year. Collisions resulting in serious injuries or fatalities went up from 2022 to 2023, as did the overall number of collisions.

What is the minimum car insurance required in Texas?

Texas requires all drivers to carry at least the following liability coverage:

- $30,000 in bodily injury liability per person

- $60,000 in bodily injury liability per accident

- $25,000 in property damage liability per accident

State minimum liability may not fully cover all of the costs if you cause a serious accident. To better protect yourself from lawsuits after an at-fault accident, consider raising your liability limits to $100,000 per person and $300,000 per accident of bodily injury liability and $100,000 in property damage liability.

Texas insurers are also required to offer personal injury protection (PIP) and uninsured motorist/underinsured motorist coverage (UM/UIM). You’re not required to carry them, but these valuable coverages are generally worth keeping.

Liability vs. full coverage: Which should you get in Laredo, TX?

Liability coverage will help pay for the other party’s property damage and medical bills if you get into an accident, but it won’t cover any of your own vehicle repairs. For that, you’ll need full coverage, which consists of:

- Collision coverage: Pays to repair or replace your car after a collision with another vehicle or object

- Comprehensive coverage: Covers damage due to theft, vandalism, fire, hail, flooding, falling objects, or a collision with an animal

It might cost more in the short term, but if replacing your vehicle would cause financial hardship, full coverage is a good investment.

The best auto insurance companies for state minimum liability coverage

These are some of the companies that offer low rates for minimum liability coverage in Laredo.

| Insurance company | Average monthly rate |

|---|---|

| Nationwide | $324 |

| Kemper | $345 |

| Amica | $556 |

| Travelers | $565 |

| Mercury | $573 |

| Clearcover | $657 |

| National General | $678 |

| Safeco | $779 |

| Infinity | $882 |

| Met360 | $995 |

The best insurance companies for full coverage

Here’s what drivers pay on average for full coverage insurance with some of the top auto insurance providers in Laredo:

| Insurance company | Full coverage |

|---|---|

| Kemper | $246 |

| Nationwide | $312 |

| Amica | $410 |

| Mercury | $436 |

| Travelers | $462 |

| Clearcover | $519 |

| Infinity | $629 |

| National General | $638 |

| Lamar General | $640 |

| Safeco | $662 |

Optional add-on coverage

Laredo drivers may benefit from adding the following coverages to their auto insurance policy:

- Uninsured/underinsured motorist coverage (UM/UIM): UM/UIM helps protect you if you’re in an accident with a driver who doesn’t have insurance or whose liability limits aren’t enough to cover your expenses. In Texas, both bodily injury and property damage UM/UIM are available.

- Personal injury protection (PIP): PIP helps pay for medical bills, lost wages, and other injury-related expenses if you or your passengers are hurt in an accident.

- Medical payments coverage (MedPay): MedPay is similar to PIP, but the coverage is limited to medical expenses for yourself and your passengers.

- Towing and labor coverage: Also called roadside assistance, towing and labor coverage will come to your aid if you run out of gas, lock your keys in your car, or need a tow in the Laredo area.

- Rental reimbursement: Rental reimbursement coverage will help pay for a rental vehicle if your car is in the shop for a covered claim.

- Gap insurance: If you have a car loan and you owe more than your car is worth, gap insurance will help pay the difference if your vehicle is totaled.

Penalties for driving without insurance in Laredo

The state of Texas takes driving without insurance seriously. Penalties for a first-time offense may include:

- Fines from $175 to $350

- Possible SR-22 requirement

If you’re convicted second or subsequent times, the consequences could include:

- Fines from $350 to $1,000

- Possible SR-22 requirement

- Possible court-ordered vehicle impoundment (180 days)5

What affects the cost of car insurance in Laredo, TX?

Your car insurance costs are highly individualized—they’re based on your driving profile, which includes information like your age, driving history, vehicle type, current insurance status, credit score, and more.

Age

In general, drivers under the age of 21 will pay the highest rates for car insurance due to their inexperience behind the wheel. Rates will stay relatively high until a driver reaches the age of 25, with drivers between the ages of 45 and 64 paying the lowest rates.

Teens and young adults

According to the CDC, teen drivers have a fatal crash rate that’s three times higher than older drivers—and insurance rates will reflect that.

| Insurance company | Monthly full coverage rate |

|---|---|

| Progressive | $203 |

| Allstate | $291 |

If you’re a parent, the best way to keep rates low for your teen or college-age driver is to keep them on your policy as long as possible. It costs significantly more for young drivers to have their own insurance plan—and as long as they still live at home, they’re eligible to be listed on your policy.

It costs around $245 a month to add a teen to your policy, but it would cost about $416 a month for them to carry their own insurance—almost 70% more.

Learn more: Find cheap car insurance for teenagers

Average rates for Laredo drivers aged 22-25

Although car insurance costs will still be high for drivers between the ages of 22 and 25, they should start to go down slightly.

| Insurance company | Monthly full coverage rate |

|---|---|

| Travelers | $85 |

| Allstate | $133 |

| Progressive | $163 |

| State Auto | $246 |

Average rates for Laredo drivers aged 26-34

Once a driver reaches the age of 26, their experience behind the wheel may contribute to a steep drop in car insurance costs

| Insurance company | Monthly full coverage rate |

|---|---|

| Nationwide | $40 |

| Travelers | $78 |

| Allstate | $109 |

| Progressive | $117 |

| State Auto | $131 |

Average rates for Laredo drivers aged 35-44

Drivers between the ages of 35 and 44 enjoy some of the cheapest rates on their car insurance on average.

| Insurance company | Monthly full coverage rate |

|---|---|

| Travelers | $53 |

| Progressive | $107 |

| Allstate | $122 |

| National General | $129 |

| State Auto | $153 |

Average rates for Laredo drivers aged 45-54

Rates continue to be low on average for drivers who are between the ages of 45 and 54.

| Insurance company | Monthly full coverage rate |

|---|---|

| Travelers | $39 |

| Progressive | $76 |

| Allstate | $103 |

| State Auto | $110 |

Average rates for Laredo drivers aged 55-64

Drivers between the ages of 55 and 64 generally pay the lowest average car insurance costs.

| Insurance company | Monthly full coverage rate |

|---|---|

| Travelers | $33 |

| Nationwide | $47 |

| Progressive | $60 |

| Allstate | $93 |

| State Auto | $119 |

Learn more: The best car insurance for seniors

Household makeup

While your car insurance premiums will go up for each car or driver you add to your policy, you may be able to get a discount for insuring multiple vehicles, which could help offset the overall price difference.

| Number of cars in household | Average annual full coverage rate |

|---|---|

| 1 | $1398 |

| 2 | $1182 |

| 3 | $1570 |

| 4+ | $2061 |

Housing situation

Auto insurance companies often offer lower rates to people who own their own homes. In addition, drivers can save by bundling their homeowners insurance with their car insurance policy, which may also contribute to the significant difference between car insurance costs for homeowners and renters.

| Average annual insurance cost | |

|---|---|

| Homeowners | $1279 |

| Non-homeowners | $2916 |

Learn more: The best home and auto insurance bundles

Credit score

According to the Consumer Federation of America (CFA), drivers with a poor credit score pay 115% more for car insurance than drivers with excellent credit, and 44% more than drivers with a fair credit score.

Here’s what those numbers look like in Laredo.

| Credit range | Average annual rate in Laredo, TX |

|---|---|

| < 600 | $1,478 |

| 601 to 699 | $1,330 |

| 700+ | $1,256 |

Vehicle

Your vehicle can have a big impact on your car insurance costs. Safe, practical vehicles generally cost the least to insure, while new cars and luxury or sports vehicles typically cost the most.

The table below looks at the average insurance costs for some of the most popular vehicles in Texas.

| Model | Minimum liability average cost | Full coverage average cost |

|---|---|---|

| Ford F-150 | $83 | $152 |

| Chevy Silverado | $86 | $166 |

| Ram 1500 | $98 | $187 |

| Toyota RAV4 | $86 | $152 |

ZIP code

When calculating rates for a certain ZIP code, insurance companies look at factors like auto thefts, average income, frequency of collisions, and more.

Here are the average car insurance rates for five Laredo ZIP codes:

| ZIP code | Average annual rate |

|---|---|

| 78045 | $1127.88 |

| 78041 | $909.13 |

| 78043 | $1139.51 |

| 78046 | $1162.96 |

| 78040 | $1273.32 |

Driving record

| Coverage type | Clean record | Violations |

|---|---|---|

| Full coverage | $1,257 | $1,294 |

| Minimum coverage | $459 | $592 |

The best Laredo car insurance companies for drivers with violations

Having violations on your record can cause your car insurance rates to go up for anywhere from 3–5 years. While your rates might not go up much for minor citations, serious violations that lead to a license suspension can have an outsized impact.

| Violation | Average monthly cost of insurance |

|---|---|

| Suspension | $218 |

| Speeding over 15 | $232 |

| Speeding under 15 | $203 |

| Other | $187 |

| Clean Record | $142 |

| Failure to Obey Traffic Sign | $76 |

SR-22 insurance in Laredo, TX

If your license is suspended due to a DUI or driving without insurance, you may be required to file an SR-22 form with the state DMV. This is a certificate verifying that you carry at least state-required liability insurance.

The violation that led to your SR-22 requirement will likely make your car insurance expensive, but it’s important not to let your coverage drop, or you’ll face additional penalties and an extension of your SR-22 period.

To help keep your car insurance costs as low as possible after an SR-22, compare car insurance quotes from companies that specialize in policies for high-risk drivers.

How to find affordable car insurance in Laredo, TX

While you can’t change many of the factors that go into calculating your car insurance costs, there are still plenty of things you can do to save.

- Shop around: The best way to know you’re getting the lowest available rate on your car insurance is to compare free quotes from at least 3–5 insurance companies.

- Increase your deductible: Increasing your deductible is an easy way to lower your car insurance premium. Just be sure to choose an amount you could pay on short notice if you had to file a claim.

- Ask about discounts: Insurance companies don’t always advertise their car insurance discounts, so ask your insurance agent if you qualify for any that you’re not already enrolled in.

- Keep a good driving record: It can take a while for violations to fall off your record, but if you avoid traffic citations, accidents, or filing insurance claims, your rates will eventually go down.

- Work with a broker: A car insurance broker like Jerry is able to shop for rates with multiple insurance companies, giving them better negotiating power to find you the best deal.

Learn more: How to shop for car insurance like a pro in 2024

FAQ

-

Who has the cheapest car insurance in Texas?

-

How much is car insurance a month in Texas?

-

How much is car insurance a month in Laredo, TX?

-

What are the top rated car insurance providers in Laredo, TX?

-

How can I save on my car insurance in Laredo?

Methodology

All premium data in this article comes from real car insurance quotes obtained through the Jerry app and analyzed by our editorial team. Jerry’s data scientists analyzed over 25 million real quotes issued to users in Jerry’s proprietary database. Jerry is partnered with 55+ insurance companies in 48 states.

Unless otherwise stated, all data represents the average of the lowest quoted price at time of writing (December 18, 2023) for a currently insured single driver with a clean driving record and a single vehicle.

Minimum coverage refers to policies with the following coverage limits:

- $30,000 bodily injury liability per person

- $60,000 bodily injury liability per accident

- $25,000 property damage liability per accident

Full coverage refers to policies that contain at least the minimum liability required in Texas, along with comprehensive and collision insurance with deductibles of either $500 or $1,000.

Sources

- https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/us-private-auto-insurance-rates-see-double-digit-jump-in-2023-77178794 ↩︎

- https://www.kgns.tv/2023/05/22/vehicle-thefts-down-laredo-according-lpd-auto-theft-task-force/https://www.kgns.tv/2023/05/22/vehicle-thefts-down-laredo-according-lpd-auto-theft-task-force/ ↩︎

- https://www.txdmv.gov/mvcpa-grantees/laredo ↩︎

- https://www.kgns.tv/2023/04/25/laredo-police-department-sees-an-increase-vehicle-theft/ ↩︎

- https://statutes.capitol.texas.gov/Docs/TN/htm/TN.601.htm ↩︎

Maria is an insurance writer with over 10 years of experience as a professional writer. Prior to joining Jerry’s editorial team in 2023, she worked at various online publications like Nimble Media, Factinate.com, and served as editor-in-chief at The Medium. She holds a double major in English and Professional Writing and Communications.

2")

Expert insurance writer and editor Amy Bobinger specializes in car repair, car maintenance, and car insurance. Amy is passionate about creating content that helps consumers navigate challenges related to car ownership and achieve financial success in areas relating to cars. Amy has over 10 years of writing and editing experience. After several years as a freelance writer, Amy spent four years as an editing fellow at WikiHow, where she co-authored over 600 articles on topics including car maintenance and home ownership. Since joining Jerry’s editorial team in 2022, Amy has edited over 2,500 articles on car insurance, state driving laws, and car repair and maintenance.

3")

As Vice President of Insurance Operations at Jerry, Josh Damico leads teams across product development, operations and carrier relations, integrating Jerry’s smart and fast car insurance customer experience with that of traditional carriers to help customers find savings and coverage. Josh’s nearly 20 years of insurance-industry experience and knowledge generate partnerships with more than 55 name-brand and specialty insurance partners that enable Jerry to serve customers with all types of vehicle and policy needs.

Previously, Josh held executive roles at Geico, where he had vast regional oversight and leadership opportunities. In his most recent role as director of sales, servicing, and underwriting, Josh developed and executed profit and growth strategy for the New England states and New Jersey.

Josh holds a bachelor’s degree in business administration and management from Medaille College.