- Boston drivers pay an average of $179 / month for full coverage

- Boston drivers pay an average of $76 / month for minimum coverage

- Average rates for Boston car insurance are higher than both the Massachusetts and US average.

- Massachusetts state law only requires 20/40/5 liability insurance, plus uninsured motorist coverage and $8,000 of PIP

Boston, Massachusetts is one of the oldest cities in the United States. Its historic cobblestone streets are home to nearly 800,000 residents, plus millions more in the surrounding metropolitan areas.

Unfortunately, the city’s narrow, winding streets weren’t designed to accommodate today’s modern vehicular traffic, or its volume. Add that to a high cost of living, punishing winter weather, and a rising rate of auto thefts, and Boston is one of the most expensive cities for car ownership—including steep car insurance costs.

Most Boston drivers pay over $2,000 per year for full coverage car insurance. But that doesn’t mean it’s impossible to find cheap car insurance in The Cradle of Liberty—you just have to know where to look.

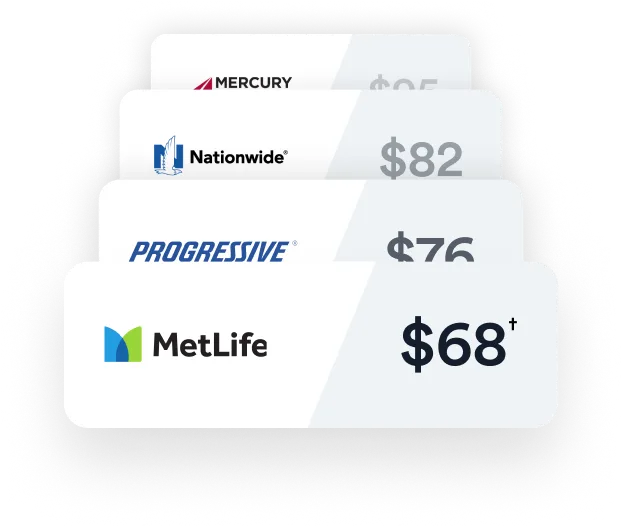

Cheapest car insurance quotes in Boston

Cheapest car insurance quotes in Boston

Hey, Bay State driver! On average, auto insurance in Boston costs about $76 per month for minimum coverage liability insurance, and about $179 per month for full coverage insurance. Boston drivers pay 14% more than the Massachusetts average.

Thousands of drivers in Boston trust Jerry Insurance Agency to help them find the best rates on car insurance from the best auto insurance companies. Jerry lets you compare and buy car insurance policies with no phone calls, no emails, and no hassle!

Below are some cheapest car insurance quotes Jerry found for our Boston customers.

|

Insurance Company

|

Premium (monthly)

|

Age

|

Zip Code

|

Car

|

Liability Limits

|

Has Full Coverage

|

|---|---|---|---|---|---|---|

| Bristol West | $115 | 32 | 02122 | Toyota Corolla Ce | State Minimum | No |

| Bristol West | $99 | 34 | 02124 | Honda Civic Lx | State Minimum | No |

| Bristol West | $56 | 30 | 02210 | Subaru Legacy 2.5I Premium | State Minimum | Yes |

| Bristol West | $110 | 25 | 02109 | Acura Tl | State Minimum | No |

| Bristol West | $113 | 26 | 02135 | Bmw 430I Gran Coupe | State Minimum | No |

Best car insurance companies in Boston

Finding the best rate for car insurance is a tricky task. Luckily, Jerry conducted a national insurance survey to uncover the best providers for drivers.

The study shows that there isn’t a “best” or “cheapest” insurance company for every driver in Boston. Rather, auto insurance companies use different algorithms to calculate insurance rates, so not every company will offer the same rate for the same driving profile—even in the same city.

In Boston, ROOT, Liberty Mutual, and National General tend to offer the cheapest rates. However, our survey revealed that USAA, Travelers, and Progressive get strong reviews from Boston drivers, too.

Here’s what Boston drivers have to say about these popular insurance providers.

| Insurance company | Overall rating | Price | Claims experience | Customer service |

|---|---|---|---|---|

| Travelers | 4.8 | 4.3 | N/A | 4.5 |

| Safeco | 4.7 | 4.6 | N/A | 4.6 |

| Progressive | 4.6 | 4.2 | 4.6 | 4.4 |

| Liberty Mutual | 3.9 | 3.4 | 3.2 | 4 |

| Geico | 3.6 | 3.1 | 3.7 | 3.8 |

How’d we get these scores?

Jerry’s experts conducted one of the largest car insurance surveys in the United States. We surveyed 15,000 policyholders, in all 50 states, over the span of 18 months. These policyholders hold insurance policies with 87 different insurance companies. We surveyed policyholders to gauge their satisfaction with their insurance carriers in: policy cost, customer service, buying and renewal experience, as well as claim experience. These scores were all reported by real customers of the insurance companies.

Best cheap car insurance quotes in Boston

Before you can get behind the wheel of a car in Boston, you must have car insurance that meets the state’s minimum insurance requirement.

Massachusetts car insurance laws require all drivers to have basic liability insurance that includes bodily injury coverage, property damage, and personal injury protection (PIP).

Cheap minimum liability insurance quotes in Boston

In order to legally hit the road, Boston drivers need to meet Massachusetts’s minimum coverage limits for bodily injury liability and property damage liability. They can be summarized as 20/40/5:

- $20,000 bodily injury liability per person

- $40,000 bodily injury liability per accident

- $5,000 property damage liability per accident

- $8,000 personal injury protection per person, per accident

- $20,000 for bodily injury per person from an uninsured motorist

- $40,000 for bodily injury per accident from an uninsured motorist

Jerry helps Boston drivers find affordable minimum liability coverage. Here are some examples of Boston car owners and how much they pay for coverage, thanks to help from Jerry.

Do you need more than minimum coverage in Boston?

Compared to other states, the minimum car insurance requirements in Massachusetts are low compared to other states. Most Boston drivers should choose to purchase insurance that exceeds the state minimum of 20/40/5.

If you’re involved in an at-fault accident, medical bills and vehicle damages can quickly exceed the state-mandated minimum. A serious crash that leaves your vehicle totaled wouldn’t be covered by state minimum coverage, and medical expenses can quickly exceed $8,000.

The bottom line: For better financial protection, Boston drivers should purchase liability coverage that exceeds the state minimum. Experts recommend 50/100/50 or 100/300/100 liability coverage—and opt for full coverage on your car.

Cheap full coverage car insurance quotes in Boston

Buying a full-coverage auto insurance policy is the easiest way to protect yourself against costs associated with repairing or replacing your vehicle if you’re involved in an accident.

A full coverage policy in Boston includes liability insurance plus comprehensive and collision coverage:

- Collision insurance: Covers the cost of damage to your vehicle caused by a collision with another object, such as another vehicle or property like a guard rail or tree. Collision coverage pays for the accident regardless of who caused it.

- Comprehensive insurance: Pays for direct and accidental damage or loss to your vehicle due to something other than a collision—theft, vandalism, fire, falling objects, larceny, or hitting an animal.

If you have a loan or lease on your car, most lenders will require you to purchase a full coverage policy that includes collision and comprehensive coverage.

|

Liability Limits

|

Has Full Coverage

|

Insurance Company

|

Premium (monthly)

|

Age

|

Zip Code

|

Car

|

|---|---|---|---|---|---|---|

| State Minimum | No | Bristol West | $115 | 32 | 02122 | Toyota Corolla Ce |

| State Minimum | No | Bristol West | $99 | 34 | 02124 | Honda Civic Lx |

| State Minimum | Yes | Bristol West | $56 | 30 | 02210 | Subaru Legacy 2.5I Premium |

| State Minimum | No | Bristol West | $110 | 25 | 02109 | Acura Tl |

| State Minimum | No | Bristol West | $113 | 26 | 02135 | Bmw 430I Gran Coupe |

The easiest and fastest way to find the cheapest car insurance for your preferred coverage option is to compare car insurance rates online.

Jerry, a top insurance agency, offers a free app that compares car insurance quotes and provides end-to-end service to customers with the help of 100+ licensed insurance agents.

Average cost of car insurance in Boston

We’ve worked with several top insurance providers in Boston, and we’ve found that the average cost for minimum liability coverage is $76 per month or $917 per year. The average cost for full coverage insurance in Boston is $179 per month or $2,150 per year.

Overall, car insurance in Boston is more expensive than both the state and national average.

| Coverage type | Boston | Massachusetts | United States |

|---|---|---|---|

| Full coverage | $2,150 | $1,948 | $1,790 |

| Minimum coverage | $917 | $903 | $740 |

Learn more: The average cost of car insurance in the US

But an average is only that—an average. Car insurance quotes are highly individualized not only because they’re based on each driver’s unique profile but also because each insurer uses its own algorithm when determining the final cost of an insurance policy.

To select the coverage and quoted price that’s best for you, just tap “Confirm your rate” to begin completing your final application. The whole process—from quoting to receiving your insurance cards—typically takes between one and two hours.

Learn more: How to shop for car insurance

Average cost of car insurance in Boston by zip code

Every city contains more than one zip code—and every zip code has a unique risk profile. This means that you and your friend, who lives in another area of Boston, could be charged totally different rates for coverage.

According to the insurance companies, one of you may be more vulnerable to auto theft, traffic accidents, or other high-risk scenarios simply due to your zip code.

| Zip Code | Average State Minimum Coverage Rate | Average Full Coverage Rate |

|---|---|---|

| 2026 | $21 | $77 |

| 2118 | $39 | $78 |

| 2119 | $28 | $113 |

| 2121 | $37 | $121 |

| 2122 | $62 | $137 |

| 2124 | $51 | $97 |

| 2126 | $70 | $80 |

| 2130 | $65 | $83 |

| 2135 | $31 | $106 |

| 2136 | $41 | $48 |

| 2215 | $117 | $133 |

Why is car insurance so expensive in Boston?

Boston’s car insurance rates are expensive for the same reasons that all Massachusetts drivers pay extra for car insurance:

- Severe winter weather: Massachusetts averages about four feet of snow each winter. The snow makes Boston’s already crowded and narrow streets even more unsafe, increasing the likelihood of accidents—and insurance claims.

- High cost of living and average income: Massachusetts is one of the most expensive states to live in, and Boston is the second most expensive city in the state. The high cost of living also means higher costs for things like healthcare, auto repairs, and other factors that can drive up insurance costs.

- Massachusetts is a no-fault state: No-fault states require drivers to purchase personal injury protection (PIP), or “no-fault insurance,” in addition to minimum liability coverage. This added expense means Massachusetts and Boston drivers often wind up paying more for coverage than drivers in other states.

But Boston is also subject to a few specific factors that raise the cost of auto coverage beyond the state average.

Traffic congestion

According to INRIX 2022 Global Traffic Scorecard, Boston ranks fourth in the world and second in the US for traffic congestion. Heavy traffic leads to an increased likelihood of accidents and insurance claims, which leads to higher overall insurance premiums.

Increased car thefts

Though nowhere near as prevalent as it was in the 1980s, car thefts are on the rise in Massachusetts, and especially in Boston. Recent FBI data indicates less than 2% of the vehicles stolen in the past three years were recovered, leading to total-loss payouts that increase average comprehensive coverage premiums for all drivers.

Car insurance quotes in Boston by rating factors

Insurance companies in Boston use many rating factors when calculating your auto insurance premium:

- Your driving record and claims history: Drivers with accidents, tickets, or other violations have higher insurance premiums than drivers with a clean record.

- Your age: Drivers younger than 25 years old will pay higher insurance rates as insurance companies consider young drivers a higher risk due to limited driving experience.

- Vehicle make and model: Luxury, high-performance, and sports cars usually have higher insurance premiums than non-luxury, less expensive vehicles.

- Vehicle location: Insurance premiums for drivers in cities are usually higher than in rural areas. Plus, rates are likely higher if you regularly park your car in a neighborhood with a higher incidence of auto insurance claims.

Cheap car insurance quotes in Boston after driving violations

Your Massachusetts driving history impacts your auto insurance quotes.

A violation on your driving record is never ideal—and it can have significant consequences for your car insurance rates. A driver with even one major or minor violation on their driving record is considered a “high-risk driver” and will pay higher insurance rates (like 30% higher!).

Cheapest car insurance in Boston after speeding ticket

In Boston, speeding tickets trigger fines—and they could increase your car insurance rate.

The minimum fine for a speeding ticket in Boston is $100. Then, drivers must pay $10 for every 10 mph over the speed limit they are caught driving.

|

Speeding Type

|

Insurance Company

|

Premium (monthly)

|

Age

|

Zip Code

|

Car

|

Liability Limits

|

Has Full Coverage

|

|---|---|---|---|---|---|---|---|

| Speeding Violation-Minor | Bristol West | $244 | 44 | 02122 | Honda Pilot Lx | State Minimum | Yes |

| Speeding Violation-Minor | Embark General | $753 | 55 | 02127 | Lincoln Mks | State Minimum | Yes |

| Speeding Violation-Minor | Embark General | $636 | 46 | 02125 | Ford C-Max Premium | State Minimum | No |

| Speeding Violation-Minor | Bristol West | $53 | 43 | 02118 | Toyota Avalon Xl | State Minimum | No |

| Speeding Violation-Minor | Bristol West | $171 | 44 | 02124 | Acura Rdx | State Minimum | No |

Cheapest car insurance in Boston after DUI

A serious driving violation like a DUI in Boston can have major implications for your car insurance premium. Penalties for DUIs are determined by the severity of the offense and the number of prior convictions in the last ten years—you’ll face more serious consequences for your second Massachusetts DUI, for instance.

Still, regardless of the penalty, insurance companies label you as a “high-risk driver.” If an insurer does agree to cover you, you’ll usually pay a much higher premium than Boston drivers without a DUI.

The best way to secure an affordable rate on Boston car insurance with a DUI on your record is to shop around for car insurance quotes from multiple providers and compare rates.

Jerry has helped several local drivers with a DUI find the lowest rates.

Cheapest car insurance in Boston after an at-fault accident

At-fault accidents on your driving record can be a big cause for an increase in your insurance rate—whether they happened in Boston or somewhere else.

Insurers look at any at-fault accidents you’ve had to determine how much of a risk you are. The more at-fault accidents you’ve had, the more high-risk you are—and the more likely they are to have to make a payout.

If you have one or more accidents on your record, you’ll likely see your premium increase when it’s time to renew your policy.

|

Accident type

|

Insurance Company

|

Premium (monthly)

|

Age

|

Zip Code

|

Car

|

Liability Limits

|

Has Full Coverage

|

|---|---|---|---|---|---|---|---|

| At Fault With No Injury | Bristol West | $180 | 43 | 02136 | Cadillac Escalade Luxury | State Minimum | No |

| Not At Fault | Bristol West | $179 | 29 | 02119 | Honda Cr-V Lx | State Minimum | Yes |

| Not At Fault | Bristol West | $255 | 38 | 02124 | Nissan Rogue S | State Minimum | Yes |

| At Fault With No Injury | Bristol West | $291 | 27 | 02124 | Bmw 328 Xi | State Minimum | No |

| At Fault With No Injury | Bristol West | $446 | 29 | 02136 | Honda Accord Ex | State Minimum | Yes |

Cheapest car insurance in Boston after other driving violations

A DUI or speeding ticket might have a significant impact on insurance rates, but so can other violations—like failing to stop at a stop sign, driving without insurance, or driving without a license. All of these can lead to higher-than-average car insurance rates until they’re no longer on your driving record.

In Boston, here are some examples of how Jerry helped drivers with violations find affordable insurance.

|

Violation

|

Insurance Company

|

Premium (monthly)

|

Age

|

Zip Code

|

Car

|

Liability Limits

|

Has Full Coverage

|

|---|---|---|---|---|---|---|---|

| Other Minor | Bristol West | $446 | 29 | 02136 | Honda Accord Ex | State Minimum | Yes |

| Other Minor | Bristol West | $180 | 37 | 02126 | Lexus Is 300 | State Minimum | No |

| Wrong Way/Wrong Lane | Bristol West | $199 | 21 | 02136 | Honda Accord Lx | State Minimum | No |

| Failure to Obey Signal | Bristol West | $156 | 25 | 02135 | Toyota Corolla L | State Minimum | No |

| Ticket Violation Not Listed | Bristol West | $183 | 24 | 02128 | Audi A6 Premium | State Minimum | No |

Cheap car insurance quotes in Boston by age

Your insurance premium is determined by several factors, but your age is a big determining factor. Drivers under 25 and over 75 tend to pay the highest rates for insurance in Boston due to a lack of driving experience and a higher risk of death and injury, respectively.

Cheapest car insurance in Boston for young drivers

Younger drivers—people under 25—pay the most for insurance of any age group in Boston. This is mainly due to a lack of driving experience that puts them at a higher risk for accidents and, therefore, a higher risk of a claim.

Do note that you may notice lower premiums for a teen driver who only has a Massachusetts provisional license. Under a provisional license, new drivers can only operate a vehicle under supervision, so they’re considered lower risk than a young driver with an unrestricted license.

Once a driver gains more experience on the road, rates will decrease, usually after 25. They remain relatively low with a clean driving record until you hit 60, when they increase again.

If you’re under 25, investing in a full coverage policy is recommended for greater financial protection.

Cheapest car insurance in Boston for senior drivers

Apart from drivers under 19, drivers over 60 have some of the highest insurance rates in Boston—despite having more driving experience.

Because seniors are at a higher risk of mortality, hospitalization, and medical expenses from car accidents and also have slower reflexes behind the wheel, they have a greater chance of being involved in an accident. A higher risk on the road means higher costs for insurers and higher insurance rates for seniors in Boston.

Cheap car insurance quotes in Boston based on insurance history

Your insurance history—how long you’ve had insurance—is one factor used to determine your insurance premium.

Insurers want to know that you haven’t had a lapse in insurance coverage, so the longer you’ve been insured continuously, the lower your premium will be. Insurance lapses label you as a “high-risk driver,” which comes with a hefty insurance rate.

Don’t panic—Jerry is here to help avoid an insurance lapse! Jerry notifies you when a payment is coming up to help you avoid missing a payment or having a lapse in insurance coverage.

Check out the table below to see how Jerry helped several Boston drivers find savings on a new insurance policy.

Cheap car insurance quotes in Boston for popular cars

The type of car you drive can influence how much you pay for your premium. Generally speaking, the higher your car’s book value, the more you’ll pay to insure it. But that’s not it—other factors associated with your car that can increase insurance rates include:

- Repair or replacement costs

- Likelihood of theft

- Safety rating

In Boston, here are some of the most popular cars:

- Nissan Maxima

- Hyundai Sonata

- Jeep Grand Cherokee

- Honda CR-V

- Toyota RAV4

- Nissan Altima

- Toyota Corolla

- Honda Civic

- Toyota Camry

- Honda Accord

Learn more: How to get car insurance before buying a car

|

Popular Car

|

Insurance Company

|

Premium (monthly)

|

Age

|

Zip Code

|

Liability Limits

|

Has Full Coverage

|

|---|---|---|---|---|---|---|

| Toyota Corolla Ce | Bristol West | $115 | 32 | 02122 | State Minimum | No |

| Toyota Corolla L | Bristol West | $55 | 30 | 02135 | State Minimum | No |

| Nissan Maxima Se | Bristol West | $61 | 29 | 02135 | State Minimum | No |

| Nissan Altima 2.5 | Bristol West | $113 | 37 | 02126 | State Minimum | No |

| Hyundai Sonata Gls | Bristol West | $285 | 37 | 02121 | State Minimum | Yes |

How to lower car insurance costs in Boston

1. Shop around and compare quotes

Insurance companies use different rules to set premiums, which are constantly changing. To ensure affordable car insurance, experts recommend comparing quotes from at least three companies and shopping for new rates every six months.

Jerry makes this process simple! In just 45 seconds, Jerry collects quotes from 55+ top insurance providers to help you find the best auto insurance coverage at the best price. And the best part? Jerry provides this service for free!

2. Hunt for car insurance discounts

Every insurance company offers a set of discounts, but the exact discount offered varies by company. Some common discounts include:

- Good driver discounts. If you have a relatively clean driving record (aka no at-fault accidents and minimal points on your license), then you might qualify for a nice discount.

- Telematics discounts. Several companies provide convenient discounts to drivers who employ telematics for tracking their driving habits. There’s even a possibility of receiving a discount merely by enrolling in the program!

- Good student discounts. If you are currently enrolled as a full-time student in high school or college and maintain a B average or higher, chances are high that you are eligible for a discount from your insurance provider.

- Bundling discounts. Bundle your home and auto insurance (or auto and renters) with the same company, and you could get a discount on both policies.

3. Increase your deductible for comprehensive and collision coverage

If you’ve got full coverage car insurance in Boston, increasing your deductible is an easy way to keep your monthly expenses low without sacrificing coverage.

FAQ

-

How much is car insurance in Boston?

-

What is the cheapest car insurance in Boston?

-

What is the best car insurance in Boston?

-

What is the minimum car insurance in Boston, Massachusetts?

1")

Sarah Gray is an insurance writer with nearly a decade of experience in publishing and writing. Sarah specializes in writing articles that educate car owners and buyers on the full scope of car ownership—from shopping for and buying a new car to scrapping one that’s breathed its last and everything in between. Sarah has authored over 1,500 articles for Jerry on topics ranging from first-time buyer programs to how to get a salvage title for a totaled car. Prior to joining Jerry, Sarah was a full-time professor of English literature and composition with multiple academic writing publications.

2")

Expert insurance writer and editor Amy Bobinger specializes in car repair, car maintenance, and car insurance. Amy is passionate about creating content that helps consumers navigate challenges related to car ownership and achieve financial success in areas relating to cars. Amy has over 10 years of writing and editing experience. After several years as a freelance writer, Amy spent four years as an editing fellow at WikiHow, where she co-authored over 600 articles on topics including car maintenance and home ownership. Since joining Jerry’s editorial team in 2022, Amy has edited over 2,500 articles on car insurance, state driving laws, and car repair and maintenance.

3")

As Vice President of Insurance Operations at Jerry, Josh Damico leads teams across product development, operations and carrier relations, integrating Jerry’s smart and fast car insurance customer experience with that of traditional carriers to help customers find savings and coverage. Josh’s nearly 20 years of insurance-industry experience and knowledge generate partnerships with more than 55 name-brand and specialty insurance partners that enable Jerry to serve customers with all types of vehicle and policy needs.

Previously, Josh held executive roles at Geico, where he had vast regional oversight and leadership opportunities. In his most recent role as director of sales, servicing, and underwriting, Josh developed and executed profit and growth strategy for the New England states and New Jersey.

Josh holds a bachelor’s degree in business administration and management from Medaille College.

*Illustration only. For all the pricing information presented in this article (including various tables), please note that not all customers find savings and the information is for illustrative purposes only. Savings depend on type of car, location, policy features, driving history and other factors. Drivers who switch through Jerry save over $70/month on average.